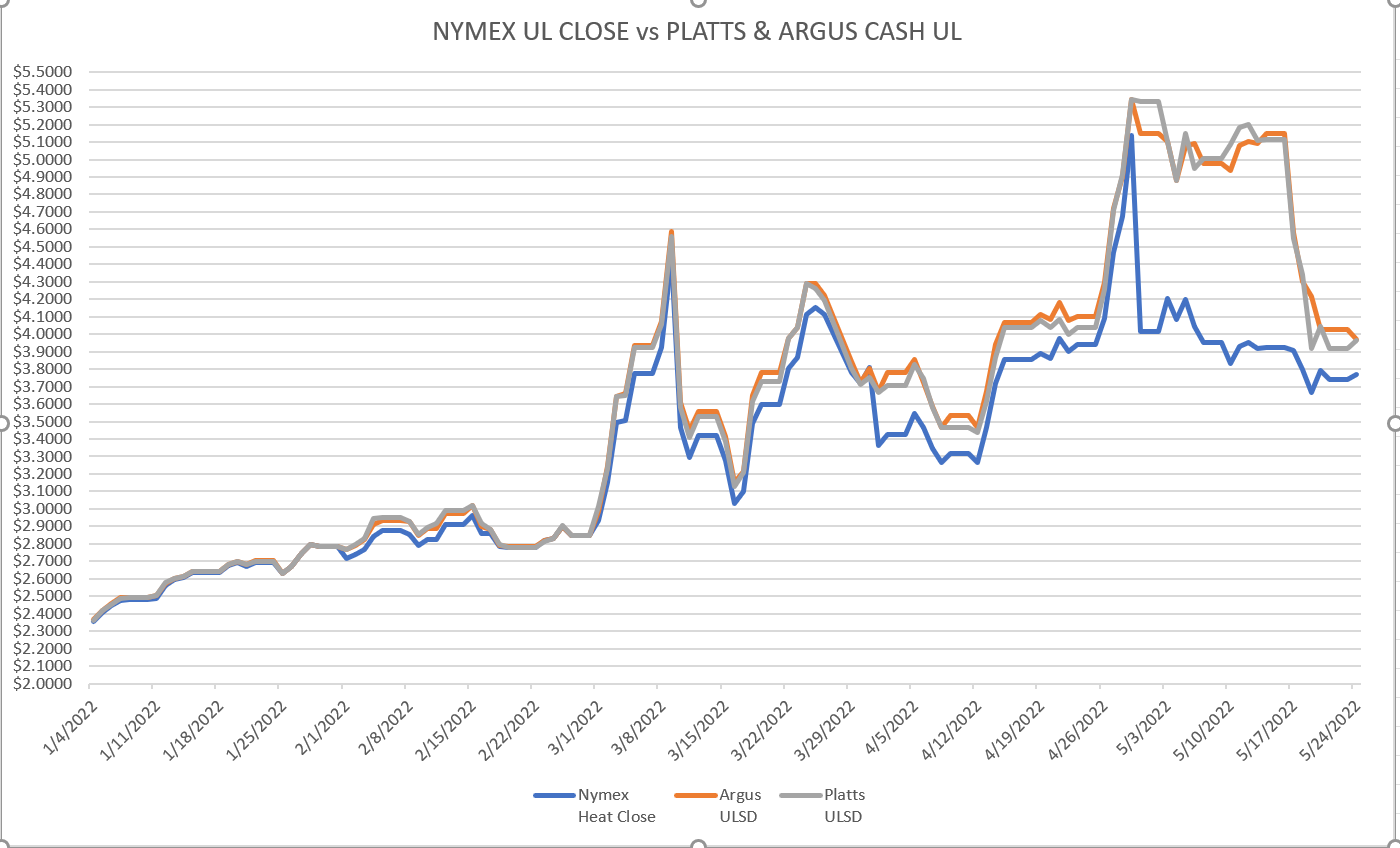

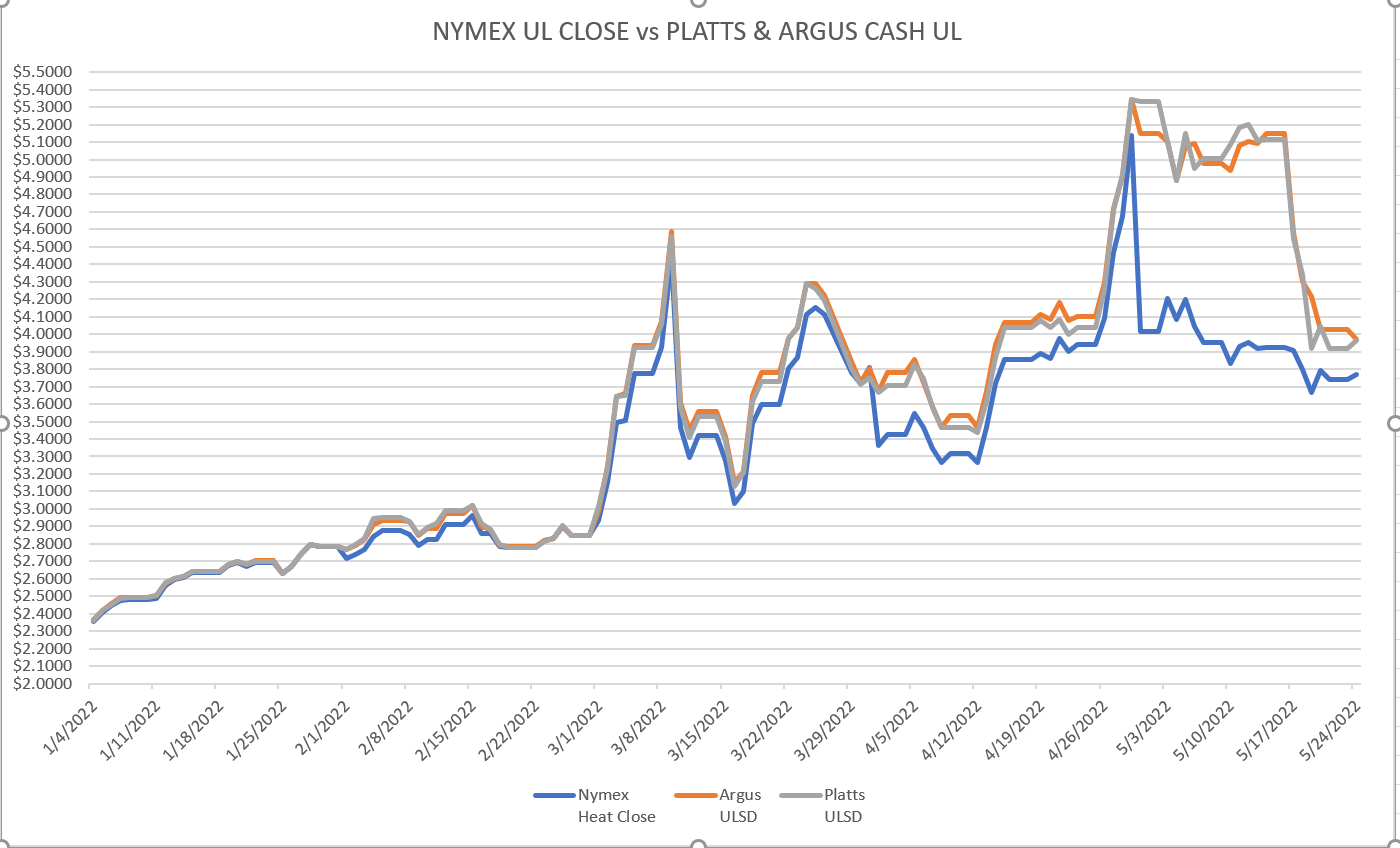

Diesel prices remain the talk of the table as they have shed over $1.00 in the last 15 days. Spot cash prices which at one point in early May were $1.25 over futures have since retraced to be roughly $.20 over. Still, by way of comparison, high to the first quarter of the year where they were pegged mostly flat to the screen. (see below).

As we mentioned, these blowouts are typically short lived - but nonetheless still very painful for many.

Northeast diesel supply appears to be slowly loosening up as the backwardation from JUNE to JULY screens sits at roughly $.13, still very high but not as high as a two weeks ago. While some suppliers are willing to take in product, it has made rack pricing extremely volatile. Typical spreads from high to low are maybe $.08 to $.10, at present, these spreads are $.40 to $1.00, not to mention figuring out who actually has product to sell. On que, refiners' distillate production is up over 5% thus far in Q2, capitalizing on the high prices and pipeline scheduling appears to be full. While this a good news for consumers, we are still at very high prices.

With China slowly reopening, expected high US gas demand and all eyes on the FED wondering if there will be another rate hike to tame inflation, I would expect it to be a while before we start to see substantially lower prices.

The suggested release of diesel reserves is not typically looked at as a fix of underlying issues, more of like taking aspirin for a tooth ache, and will likely not have much of an effect on pricing.