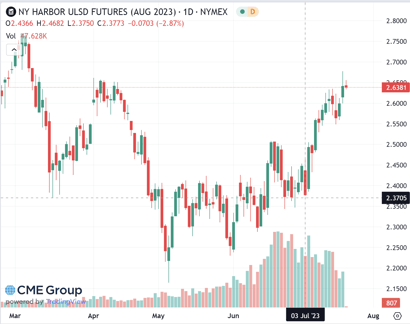

Fuel prices sit about $.30 higher today than the beginning of the month as we broke out of the comfortable range in MAY through JUNE. The three week rally can mainly be tied to production cuts, unpredictable inventory reports and mostly an optimistic view on the overall health of the US economy. The bright side is we are over $1.00 lower than this time last year. The question remains, does this rally have any legs?

In terms of production, it is a fine line where re-emerging producers such as Venezuela, Iran, and US shale jump in heavy to take advantage of the higher market prices. And ultimately, do those barrels have any affect on the overall supply picture and will that additional product push prices down? Personally, I think the real key lies in the demand picture. Diesel consumption is down roughly 3% year over year, may not seem like a lot but it is noticeable. Gasoline is actually up versus last year, but again, that may still be lingering COVID related adjustments.

With major National freight carriers all seeing volumes down significantly this year, and one facing bankruptcy, it seems likely that diesel demand will remain soft through the end of the year. We could, possibly retrace $.30 to $.50 in value should this maintain. (special note: SPR Crude is still about 150mbls lower than last year)

We are in this odd place as some businesses are flat out and others are maintaining. How much of that is staffing related is tough to tell. Being able to pivot once again may be crucial in the coming months. Having a supplier with product, trucks, staff, and multiple delivery options to meet all your fuel and lubricant needs should be a top priority as we move into the second half of the year. As always, feel free to reach out to discuss your specific operation. (You can reach out by phone, or schedule a call at a good time for you using this link: Schedule a Call )